Content

Tangible capital asset means an asset that has physical substance, more than minimal value, and is expected to be held by an enterprise for continued use or possession beyond the current accounting period for the services it yields. Immediate-gain actuarial cost method means any of the several actuarial cost methods under which actuarial gains and losses are included as part of the unfunded actuarial liability of the pension plan, rather than as part of the normal cost of the plan. Home office means an office responsible for directing or managing two or more, but not necessarily all, segments of an organization. It typically establishes policy for, and provides guidance to, the segments in their operations. It usually performs management, supervisory, or administrative functions, and may also perform service functions in support of the operations of the various segments. An organization which has intermediate levels, such as groups, may have several home offices which report to a common home office.

TheAUDITORmust perform tests of controls over aperiodof time that is adequate to determine whether, as of the date specified inmanagement’s report, the controls necessary for achieving the objectives of the control criteria are operating effectively. A pricing method that identifies the price at which a product will be competitive in the marketplace, identifies the minimum desiredPROFITto be made on the product, and computes a target cost for the product by subtracting the desired profit from the competitiveMARKET PRICE.

Indirect Labor Costs

This evidence of a thorough analysis and potentially a legal opinion may be necessary to support a company’s classification of retainage as a receivable. This article contains general legal information but does not constitute professional legal advice for your particular situation. The Law Dictionary is not a law firm, and this page does not create an attorney-client or legal adviser relationship. If you have specific questions, please consult a qualified attorney Cost in Excess of Billings Law and Legal Definition licensed in your jurisdiction. You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

Actual interest cost in lieu of the calculated imputed cost of money is unallowable. The estimated facilities capital cost of money is specifically identified and proposed in cost proposals relating to the contract under which the cost is to be claimed. Contributions by the contractor in any oneyear that exceed the deductibility limits of the Internal Revenue Code for that year are unallowable. This paragraph applies to all executive agency contracts awarded on or after June 24, 2014, and any subcontracts thereunder. All employee compensation limit for contracts awarded on or after June 24, 2014. The costs are paid to an insurer, provider, or other recipient for current year benefits or premiums.

Cost Plus Fixed Percentage Contract

Payments to employees under agreements in which they receive special compensation, in excess of the contractor’s normal severance pay practice, if their employment terminates following a change in the management control over, or ownership of, the contractor or a substantial portion of its assets. A base period for allocating indirect costs is the cost accounting period during which such costs are incurred and accumulated for allocation to work performed in that period. A cost is reasonable if, in its nature and amount, it does not exceed that which would be incurred by a prudent person in the conduct of competitive business. Reasonableness of specific costs must be examined with particular care in connection with firms or their separate divisions that may not be subject to effective competitive restraints. No presumption of reasonableness shall be attached to the incurrence of costs by a contractor. If an initial review of the facts results in a challenge of a specific cost by the contracting officer or the contracting officer’s representative, the burden of proof shall be upon the contractor to establish that such cost is reasonable. Actuarial accrued liability means pension cost attributable, under the actuarial cost method in use, to years prior to the current period considered by a particular actuarial valuation.

What is cost in excess of billings on long term contracts?

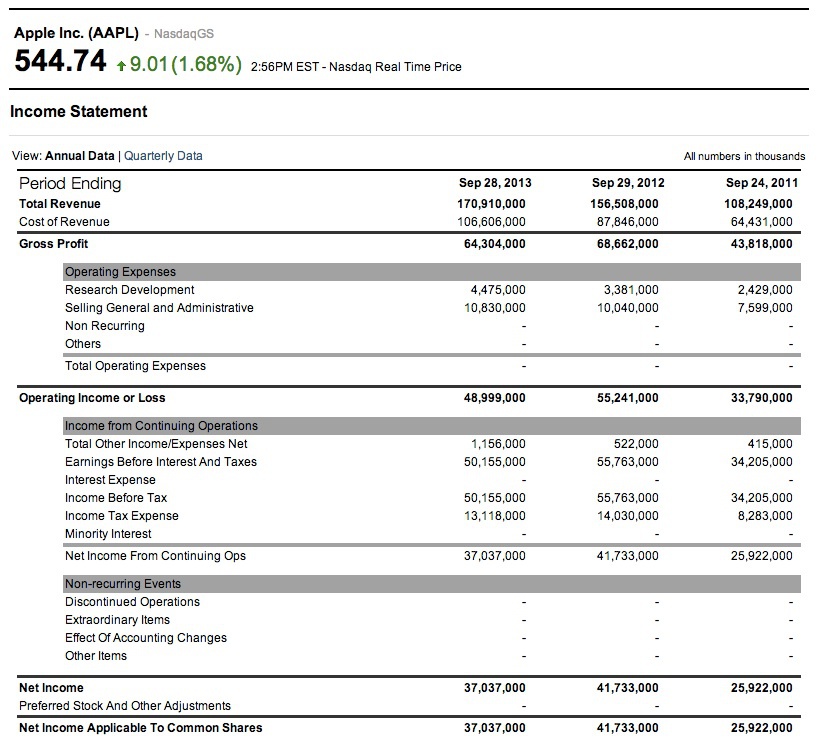

Cost in Excess of Billings, in percentage of completion method, is when the billings on uncompleted contracts are less than the income earned to date. These under-billings result in increased assets.

“Forestry materials” means materials derived from the practice of planting and caring for forests and the management of growing timber where such materials come from short-rotation woody crops that are less than ten years old, sustainably managed forests, wood residues, or forest thinnings. Any advertising purchased with public money by a state official for the same purpose that, in the aggregate, exceeds fifty thousand dollars during the fiscal year, shall be subject to controlling board approval. Paragraphs and of this section apply for taxable years beginning on or after November 20, 2018. For any taxable year that both begins before November 20, 2018 and ends after November 20, 2018, the IRS will not challenge return positions consistent with all of paragraphs and of this section. Except as provided in , , and of this section, the effective dates for this section are provided in paragraph of this section.

Cost Accounting

For voice calls, we round up any fraction of a minute to the next full minute. Depending upon your Rate Plan, data usage may be rounded at the end of each data session, at the end of your billing cycle, and/or at the time you switch data plans. You may be charged for more than one call/message when you use certain features resulting in multiple inbound or outbound calls/messages (such as call forwarding, call waiting, https://online-accounting.net/ voicemail, conference calling, and multi-party messaging). You will be charged for text, instant or picture messages, and email whether read or unread, sent or received, solicited or unsolicited. We use filters to block spam messages, but we do not guarantee that you will not receive spam or other unsolicited messages. Most usage and Charges incurred during a billing cycle will be included in your bill for that cycle.

Additionally, P uses the de minimis direct labor costs rule under paragraph of this section. P does not capitalize vacation pay or holiday pay to property produced or property acquired for resale in its financial statement but does capitalize all other direct labor costs to such property in its financial statement. On its 2018 financial statement, P incurs $3,500,000 of total direct labor costs, including $110,000 of vacation pay costs and $10,000 of holiday pay costs. For federal income tax purposes, P incurs $150,000 of vacation pay costs and $18,000 of holiday pay costs in the taxable year. P’s uncapitalized direct labor costs are $120,000 ($110,000 of vacation pay plus $10,000 of holiday pay). For purposes of the five percent test in paragraph of this section, P’s uncapitalized direct labor costs are 3.43% of total direct labor costs ($120,000 divided by $3,500,000).

ABONDthat is usually not registered with the issuingCORPORATIONbut instead bearsinterestcoupons stating the amount of INTEREST due and the payment date. INTEREST rateon aDEBT SECURITYtheISSUERpromises to pay to the holder untilmaturity, expressed as an annual percentage ofFACE VALUE. DEBT instrumentissued by a privateCORPORATION, as distinct from one issued by a government agency or a municipality. Tests directed toward the design or operation of aninternal controlstructure policy or procedure to assess its effectiveness in preventing or detectingmaterialmisstatements in a financialreport. AUDITOR’S receipt of a written or oral response from an independent third party verifying the accuracy of information requested.